The Week in Review: January 20, 2025

Despair to Jubilation and Beyond

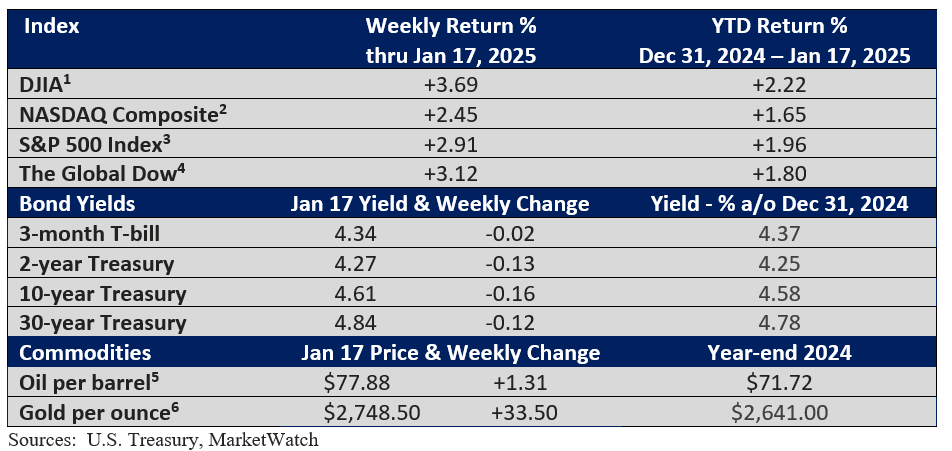

It’s prudent to cautiously eye rapid changes in market sentiment caused by short-term traders. A week ago, our summary focused on a strong jobs report, rising bond yields, and general concerns about inflation. There was a sense of despair among traders at week’s end.

With the arrival of a new week, investors shifted their focus from what felt like a suspenseful thriller to a lighthearted, family-friendly feature that even concluded with a Hallmark ending.

What happened? Short-term traders were on the edge of their seats on Wednesday, awaiting the release of the December Consumer Price Index (CPI) by the U.S. Bureau of Labor Statistics.

While the headline CPI rose a slightly higher than expected 0.4%, the core CPI, which excludes food and energy, rose a slightly smaller than expected 0.2%. Major news outlets, including the Wall Street Journal, published the consensus forecast.

Call it a major relief rally, as longer-term Treasury bond yields plummeted, and stocks rallied sharply. The headline CPI is important, but investors were solely focused on the core CPI.

The graph illustrates that the road to a lower inflation rate has been bumpy. While progress has slowed, the peaks and valleys in the 4-month moving average remain in a downward trend.

Further, last week was the unofficial kickoff to Q4 earnings season. According to LSEG, the early read is favorable, as companies are topping analyst estimates by a wide margin on average.

Separately, the inauguration of Donald Trump on Monday marks the beginning of a new chapter for our nation. It's early, but the new president could issue a flurry of executive orders, which may support (deregulation) or dampen enthusiasm (hefty tariffs) for equities, at least in the short term.

Over the longer term, however, economic fundamentals—including the economy, corporate earnings, and interest rates—influence markets.

Ultimately, it’s important to stay focused on your financial goals, maintain diversification, understand your financial comfort zone, and be mindful that volatility, when it arises, shouldn’t distract you from your unique investment plan and goals.

Market Summary

TWO FOR THE ROAD

When stocks finish January in positive territory, the rest of the year sees gains 79% of the time, with a median increase of 11.5%. When January is negative, the likelihood of gains drops to 58%, and the average increase is just 2.4%. - Barron’s, January 2, 2025

Over the last decade, fueled by AI, US oil producers have pumped 60% more oil daily with 40% fewer workers. By extracting more oil while reducing expenses, they’re lowering the costs to drill profitably. In the Permian Basin, the break-even price for oil producers has fallen to $40 a barrel from over $90 in 2012. - The Barron’s Daily November 26, 2024

Please do not hesitate to contact me with any questions or concerns.

I hope you have a great week!

Bill Stordahl, CFP®

Managing Director

Stordahl Capital Management

Stordahl Capital Management, Inc is a Registered Investment Adviser. This commentary is solely for informational purposes and reflects the personal opinions, viewpoints, and analyses of Stordahl Capital Management, Inc. and should not be regarded as a description of advisory services or performance returns of any SCM Clients. The views reflected in the commentary are subject to change at any time without notice. Nothing in this piece constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Advisory services are only offered to clients or prospective clients where Stordahl Capital Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Stordahl Capital Management unless a client service agreement is in place. Stordahl Capital Management, Inc provides links for your convenience to websites produced by other providers or industry-related material. Accessing websites through links directs you away from our website. Stordahl Capital Management is not responsible for errors or omissions in the material on third-party websites and does not necessarily approve of or endorse the information provided. Users who gain access to third-party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from the use of those websites. Please note that trading instructions through email, fax, or voicemail will not be taken. Your identity and timely retrieval of instructions cannot be guaranteed. Stordahl Capital Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

1. The Dow Jones Industrials Average is an unmanaged index of 30 major companies which cannot be invested into directly. Past performance does not guarantee future results.

2. The NASDAQ Composite is an unmanaged index of companies which cannot be invested into directly. Past performance does not guarantee future results.

3. The S&P 500 Index is an unmanaged index of 500 larger companies which cannot be invested into directly. Past performance does not guarantee future results.

4. The Global Dow is an unmanaged index composed of stocks of 150 top companies. It cannot be invested into directly. Past performance does not guarantee future results.

5. CME Group front-month contract; Prices can and do vary; past performance does not guarantee future results.

6. CME Group continuous contract; Prices can and do vary; past performance does not guarantee future results.