The Week in Review May 9, 2022

Biggest Rate Hike in Over 20 Years, but More Aggressive Path Quashed

As widely expected, the Federal Reserve hiked its key lending rate, the fed funds rate, by 50 bp (basis points, 1 bp = 0.01%) to a range of 0.75—1.00%. It is the first 50 bp rate hike in over 20 years. As it detailed in its statement, the Fed will also begin letting some of the bonds it acquired in the pandemic run off its balance sheet starting in June. This was also expected.

The rate increase was no surprise, and there wasn’t an immediate market reaction. Instead, it was comments that came in the press conference that moved the market.

In response to a question, Powell said a 75 bp rate hike “is not something the committee is actively considering.” That was a surprise. He could have kept his options open.

Instead, 50 bp over the next two meetings “should be on the table.” Removing 75 bp sparked a big rally on Wednesday, but Powell may have inadvertently set the stage for Thursday’s selloff.

By pouring cold water on a 75 bp rate hike, the Fed may have sparked Thursday’s turbulent jump in bond yields. A slightly less hawkish message is the opposite of what is needed to combat inflation, and bond investors reacted.

The Fed may be looking at the shrinking balance sheet in lieu of bigger rate hikes. Powell did not elaborate.

Other notable remarks: Powell said he sees a “good chance to have a soft or softish economic landing.” Softish? He didn’t explain. Did he mean a mild recession? It’s not clear.

He also said the Fed “won’t hesitate to deliver” higher rates, and tackling inflation “is not going to be pleasant.” Yet, 75 bp appears to be off the table.

Broader View

Today, the Fed’s focus is on inflation. It should have raised rates last year, it is behind and is trying to catch up, and market sentiment reflects today’s mood.

Historically speaking, rates remain low, but they are becoming less supportive of growth and may eventually restrict growth. That seems to be where the Fed is headed.

The Fed can slow overall demand in the economy, and slower demand for goods and services can slow inflation. But supply issues like oil, natural gas, wheat, semiconductors, and China Covid lockdowns are outside its control.

What might it take to reduce bearish sentiment?

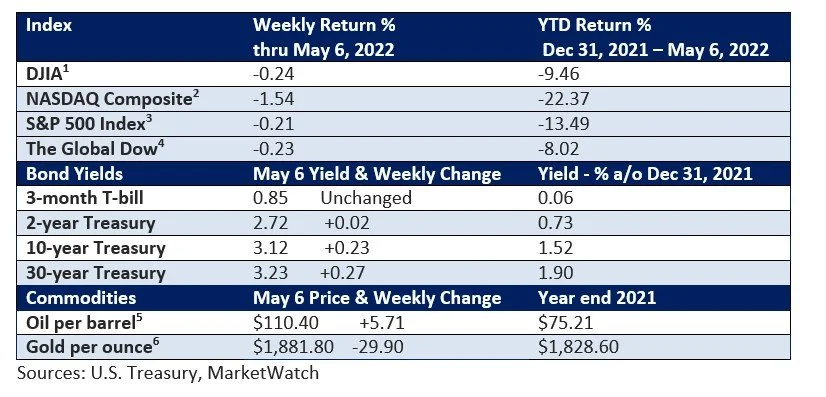

The S&P 500 Index is down 14% from its Jan. 3 peak (St. Louis Fed Reserve). Since 1980, the average annual peak-to-trough pullback in the index is 14%, according to LPL Research. While stocks climb the ladder over the long-term, volatility isn’t unusual. Yet, it can be unnerving.

What’s needed? No one has the tools in their toolkit to consistently call tops and bottoms. And what might be helpful can shift over time.

Today, investors want to see signs that inflation is peaking and on a downward path. Why? Slower inflation reduces the need for steep rate increases, which have created stiff headwinds for stocks.

Powell said the Fed is seeing some evidence that core inflation, which excludes food and energy, “is perhaps reaching a peak or flattening out. We want to see more than just some evidence.”

But the Fed is hoping to slow inflation without tipping the economy into a recession. They will need skill and some luck. The strong dollar could help with the price of imported goods, but the economy needs fewer obstructions in the supply chain.

If you have any questions or concerns, please don’t hesitate to let me know.

Two for the Road

Global gross domestic product in 1900 was $3.4 trillion. In 2020 that figure was $112.7 trillion. During the same 120-year period, the world population grew from 1.6 billion to 7.8 billion. Less than five times as many people produced more than 33 times as much output. - The Wall Street Journal, April 22, 2022

A new survey found that 32% of U.S. adults favored scientists attempting to bring back extinct animals. Of those, 39% favored giving the Dodo another chance, 20% the Saber-tooth tiger, and 10% backed reviving the Tyrannosaurus Rex. - YouGovAmerica, April 22, 2022

This commentary reflects the personal opinions, viewpoints and analyses of the Stordahl Capital Management, Inc. employees providing such comments, and should not be regarded as a description of advisory services provided by Stordahl Capital Management, Inc. or performance returns of any Stordahl Capital Management, Inc. Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this piece constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Accessing websites through links directs you away from our website. Stordahl Capital Management is not responsible for errors or omissions in the material on third party websites and does not necessarily approve of or endorse the information provided. Users who gain access to third party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from the use of those websites. Please note that trading instructions through email, fax or voicemail will not be taken. Your identity and timely retrieval of instructions cannot be guaranteed. Stordahl Capital Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

1. The Dow Jones Industrials Average is an unmanaged index of 30 major companies which cannot be invested into directly. Past performance does not guarantee future results.

2. The NASDAQ Composite is an unmanaged index of companies which cannot be invested into directly. Past performance does not guarantee future results.

3. The S&P 500 Index is an unmanaged index of 500 larger companies which cannot be invested into directly. Past performance does not guarantee future results.

4. The Global Dow is an unmanaged index composed of stocks of 150 top companies. It cannot be invested into directly. Past performance does not guarantee future results.

5. CME Group front-month contract; Prices can and do vary; past performance does not guarantee future results.

6. CME Group continuous contract; Prices can and do vary; past performance does not guarantee future results.