The Week in Review: November 15, 2021

The Case for “Transitory” Loses Ground

For much of the year, we have listened to Federal Reserve officials argue that the surge in inflation is “transitory.” Transitory simply means temporary. Yet the latest inflation numbers suggest the Fed’s line of reasoning is losing some of its punch.

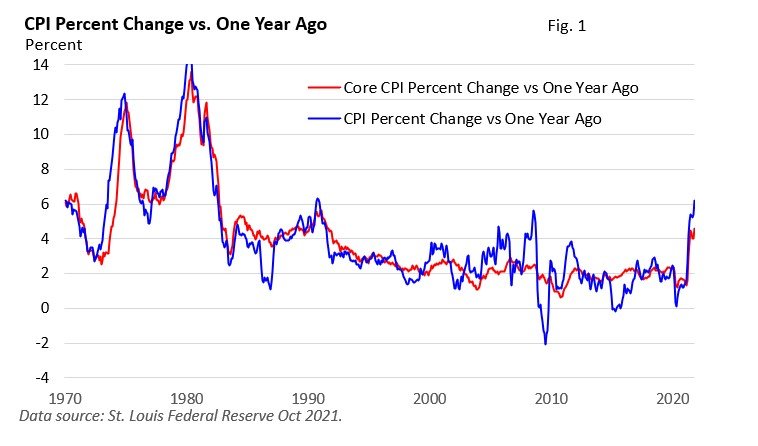

In October, the Consumer Price Index rose 6.2% versus one year ago, according to the U.S. Bureau of Labor Statistics (BLS). Yank out food and energy and the core CPI rose 4.6%. Both were the highest readings in 30 years—see Figure 1.

On a monthly basis, the CPI was up 0.9%, while the core CPI rose 0.6%.

In the late 2000s, the rise in inflation was due primarily to soaring gasoline prices. While energy costs are up sharply, today’s increases are much more broad-based.

Categories that fall under services have lagged but are starting to show signs of heating up. However, it has been the price of everyday goods that has jumped sharply.

Even if we remove used cars (up 26% versus one year ago), we have been experiencing sharp increases in the price of goods—see Figure 2.

Against the backdrop of cheap money, it mostly boils down to a few items. Pandemic stimulus has lifted spending on goods and fueled demand at a time when production bottlenecks are hampering the supply of goods. The result: Prices are going up.

While we experienced a lull in Q3 economic growth, activity has accelerated sharply as Q4 gets underway. Yet the University of Michigan’s consumer sentiment survey hit a 10-year low in its mid-November reading. It seems like a disconnect.

U of Michigan’s chief economist blamed the drop in confidence on an “escalating inflation rate and the growing belief among consumers that no effective policies have yet been developed to reduce the damage from surging inflation.”

In other words, most consumers are fretting over higher prices.

Perhaps we’ll look back late next year and take note of slowing inflation, and the Fed can take a victory lap. The Producer Price Index, which measures wholesale prices, has moderated slightly, per the U.S. BLS. But October’s CPI suggests inflation isn’t slowing anytime soon.

If you have any questions or concerns, please don’t hesitate to let me know.

Two for the Road

This year, the government collected $627 billion more in tax revenue than it did in fiscal 2020, pulling in a record-high $4.05 trillion. —TheRightFacts

During the Fed’s last taper, the S&P 500 gained 15% in a broad advance. —CNBC, November 5, 2021

This commentary reflects the personal opinions, viewpoints and analyses of the Stordahl Capital Management, Inc. employees providing such comments, and should not be regarded as a description of advisory services provided by Stordahl Capital Management, Inc. or performance returns of any Stordahl Capital Management, Inc. Investments client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this piece constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Accessing websites through links directs you away from our website. Stordahl Capital Management is not responsible for errors or omissions in the material on third party websites and does not necessarily approve of or endorse the information provided. Users who gain access to third party websites may be subject to the copyright and other restrictions on use imposed by those providers and assume responsibility and risk from the use of those websites. Please note that trading instructions through email, fax or voicemail will not be taken. Your identity and timely retrieval of instructions cannot be guaranteed. Stordahl Capital Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

1. The Dow Jones Industrials Average is an unmanaged index of 30 major companies which cannot be invested into directly. Past performance does not guarantee future results.

2. The NASDAQ Composite is an unmanaged index of companies which cannot be invested into directly. Past performance does not guarantee future results.

3. The S&P 500 Index is an unmanaged index of 500 larger companies which cannot be invested into directly. Past performance does not guarantee future results.

4. The Global Dow is an unmanaged index composed of stocks of 150 top companies. It cannot be invested into directly. Past performance does not guarantee future results.

5. CME Group front-month contract; Prices can and do vary; past performance does not guarantee future results.

6. CME Group continuous contract; Prices can and do vary; past performance does not guarantee future results.